Price stability justified for 2019

With subdued global milk supply growth, empty SMP intervention stores, a Brexit threat delayed well past peak and reasonable demand from China and Asia, all indicators point to stable dairy market prices after some earlier easing – which should spell stable milk prices. So, why should co-ops at this point commit to no further milk price cuts for 2019?

Supply growth negative in February

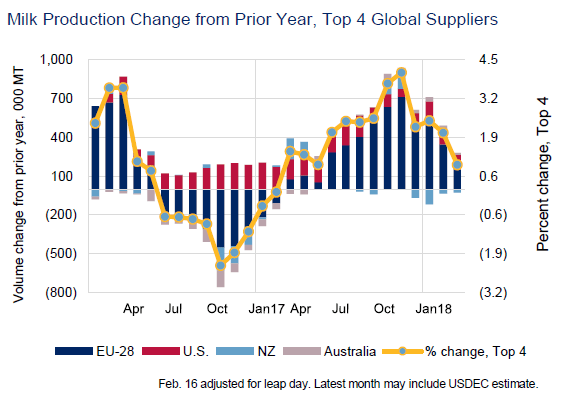

Worldwide milk production by the main exporting nations has gone into negative territory in February (see graph below).

This reflects the continued severe downturn in Australian supplies (down 12.6% for February, and by 6.4% for the June to February period).

Also down are EU supplies: for the combined January and February period, they were 0.6% down in volume, with Germany, France and the Netherlands well back. Exceptions worthy of note are of course Ireland and Poland.

US output was only up 0.2% for February, and growth there, which had been between 1.5% and 2% every month, year on year, has been much more subdued in recent months.

New Zealand had been forging ahead strongly through their October peak. However, it started the calendar year in reverse, with February supplies down 0.12%, and March supplies well back by 7.4%!

With global output growth stable to negative, markets have taken good note of likely scarcer supplies later this year – which has translated most clearly into 10 consecutive positive GDT auctions, the last one earlier this week.

Source: USDEC

In their Quarter 1 Dairy Quarterly report, Rabobank do expect that lower output growth will remain the form for much of 2019, and they even go so far as to suggest that low growth might persist into 2020. The main reason they give for this is the fall in milk prices over recent months to levels in most countries below production costs.

This expectation leads them to forecast stable milk prices for the first 2 quarters of 2019, possibly followed by some price improvements from the end of quarter 2.

Source: Rabobank

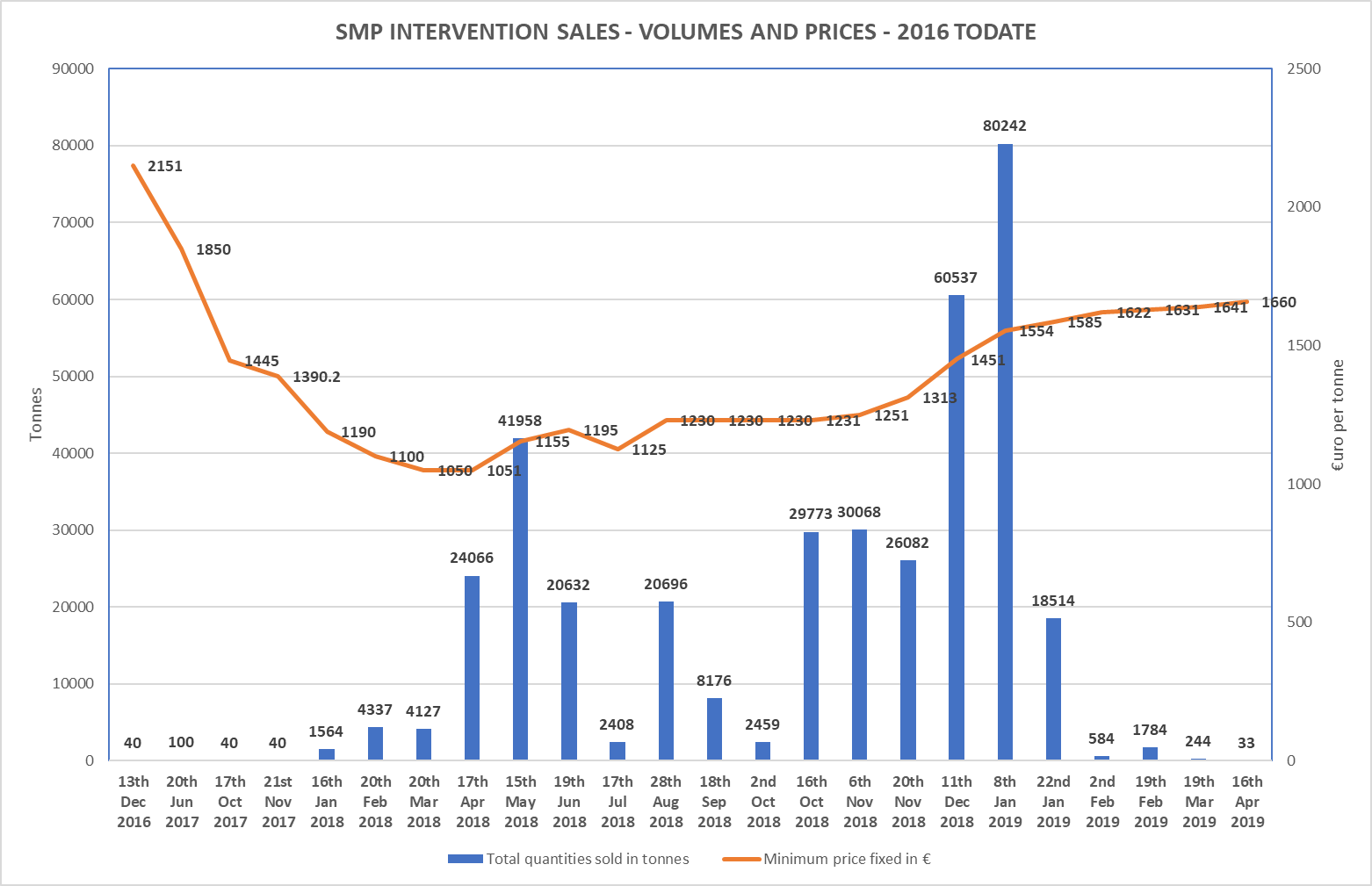

SMP intervention stocks empty

After the last sale of SMP out of intervention on 16th April, 33 tonnes at a minimum price of €1660/t, there is now only 1106t left for sale. All of this will be made available for tender on 21st May.

A total of 378,504t have been sold out of intervention since the sales began in 2016. With only just over 1000t left, stocks are quasi empty. However, it is likely that some of this product has still to be absorbed in the market place.

Based on EU MMO

GDT scores 10 consecutive increases

Since early December 2018, all 10 GDT auctions have scored positive index increases, the latest one on 16th April at +0.5%.

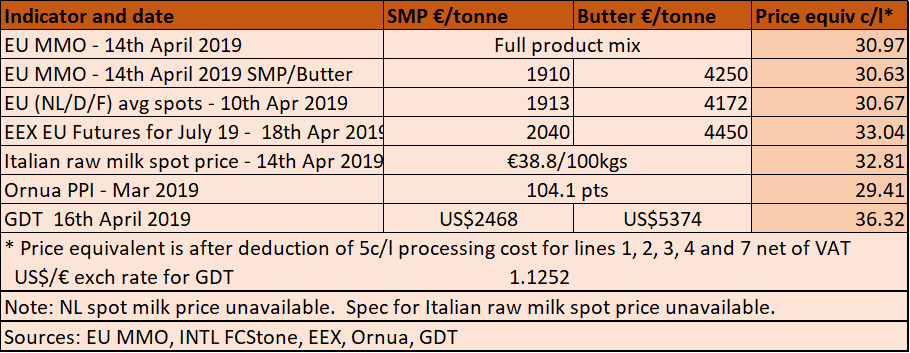

The index has increased 28% since late November. Butter prices, at US $5544/t are almost €800 dearer at current exchange rates than the most recent average EU butter prices. SMP is almost €300/t dearer than EU product prices. As a result, the latest SMP and butter prices would yield an “Irish” milk price of 36.32c/l + VAT.

Source: GDT

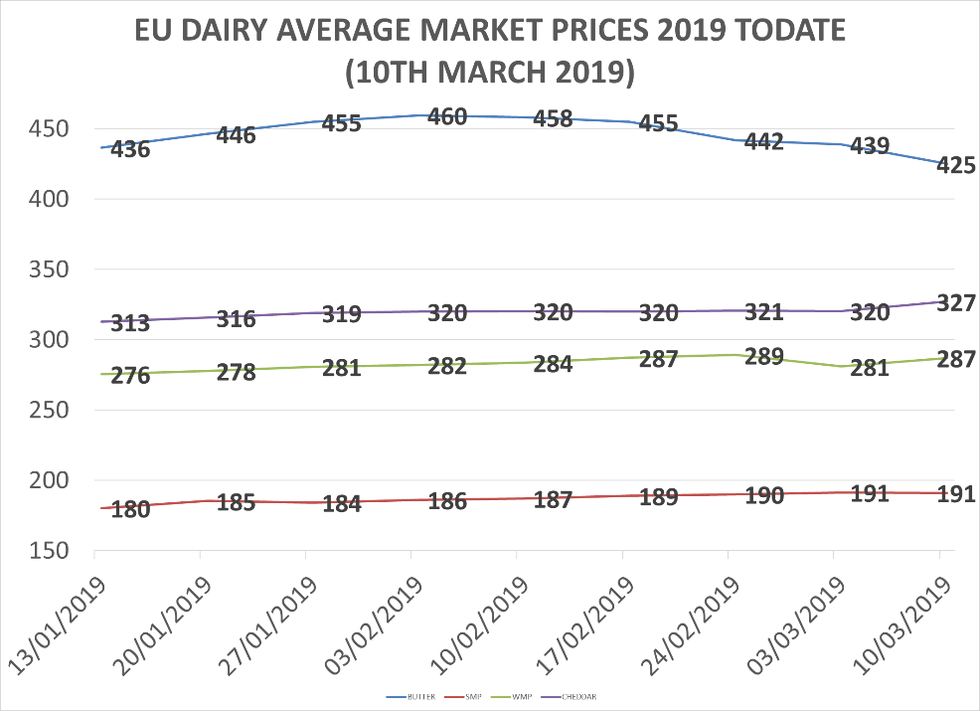

EU powder prices stable to firmer since January

There has been a divergence between price trends in GDT and global international markets, which have seen strong growth in butter and powder prices, and EU prices.

EU butter prices have been slipping early this year, yet remain above €4000/t, and so at historically high levels. Whey powder prices have also been slipping somewhat.

However, SMP and WMP has both been firming since January, reflecting strong exports and the emptying of intervention stocks.

Cheddar cheese prices have been stable to slightly firmer, despite the Brexit fears.

Based on EU MMO

Brexit threat postponed, but…

After two deadline postponements for Brexit from 29th March to 12th April, then to 31st October, the reality is that the possibility (never to be excluded) of a hard Brexit has been postponed to a date beyond peak milk production. This is positive in that the trading conditions (no tariffs, no delay or paperwork at the border…) remain unchanged for longer than might have been the case with a no deal crash out this spring.

However, we hear from cheese traders that, with significant stockpiling ahead of the first 29th March deadline, and with strong increases in UK milk (+2.7% for February) and cheese production (+2.7% in the last 12 months), freshly produced UK cheddar is now competing with stockpiled Irish. Quite a bit of retail promotions (i.e. competition based on reduced prices) is being reported.

Oil prices strengthening importing countries’ purchasing power

Since January, the Brent crude oil price has moved from around US$63 per barrel to a current US$72.

Higher oil prices always correlate to stronger dairy prices, because they increase the export earnings of many of our customer countries, such as the Middle East, North Africa and the likes.

With the trend currently up, this coincides with other factors to suggest better or at least more stable dairy prices over the coming weeks and months.

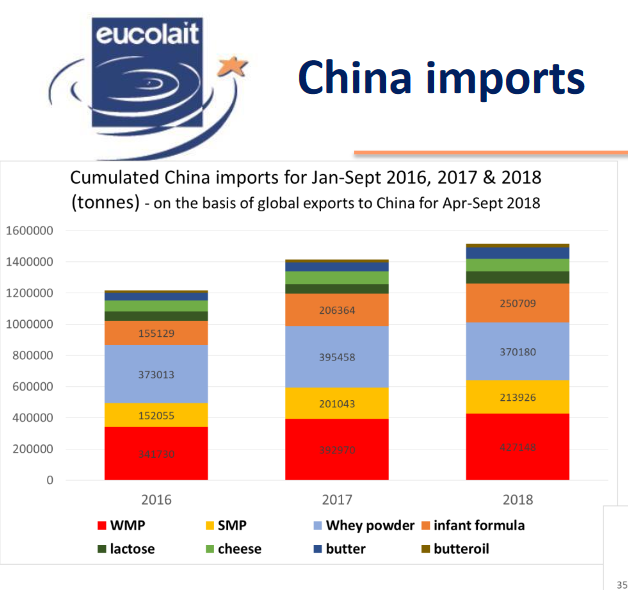

Massively increased EU powder exports – SE Asia, MENA and Africa feature strongly

EU SMP export for Jan/Feb 2019 were a whopping 37% above exports for the same period last year. This follows a full year performance up 5.4% in 2018 compared to 2017.

China, which has imported 172% more powder in Jan/Feb 19 than in the previous year, is closing in on Algeria as our main market for SMP, but all the main destinations of SE Asia, the Middle East and Africa above and below the Sahara have clocked up massive increases into the early months of 2019.

Source of both above: EU MMO

Cheese exports for the same period were strongly up too, by 7% compared to the same period last year.

This follows a historical year in which 832,000t of cheese were exported from the EU, the highest level in at least 7 years.

Demand from China continues strong

China is predicted by Rabobank in its 1st 2019 quarterly dairy report as remaining a strong feature in international dairy demand. Domestic supplies will remain short of demand, and Rabo predicts accelerated import activity in the second half of the year.

Source: CLAL.it

Return levels would justify holding milk prices – and co-ops must signal end of price cuts for 2019

The current average milk price paid by co-ops for February is around 30-31c/l + VAT. The returns for the main indicators outlined below about match this.

With farmers in need of every cent, as peak month cheques arrive, to catch up with the massive bills accumulated in 2018, it is essential that co-ops would signal clearly to farmers that this is the end of milk price cuts for 2019.