With global milk output growing at much slower rates (just over 1% for March, the level analysts believe is required to rebalance markets), intervention SMP stock shifting more readily, and international commodity price indices on the up, it looks like we may have seen the last of the (base) milk price cuts for 2018.

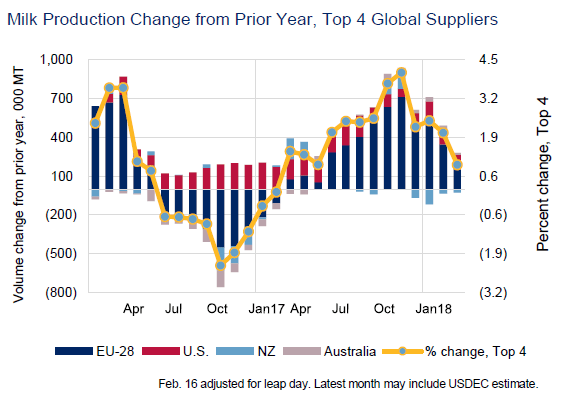

Source: USDEC

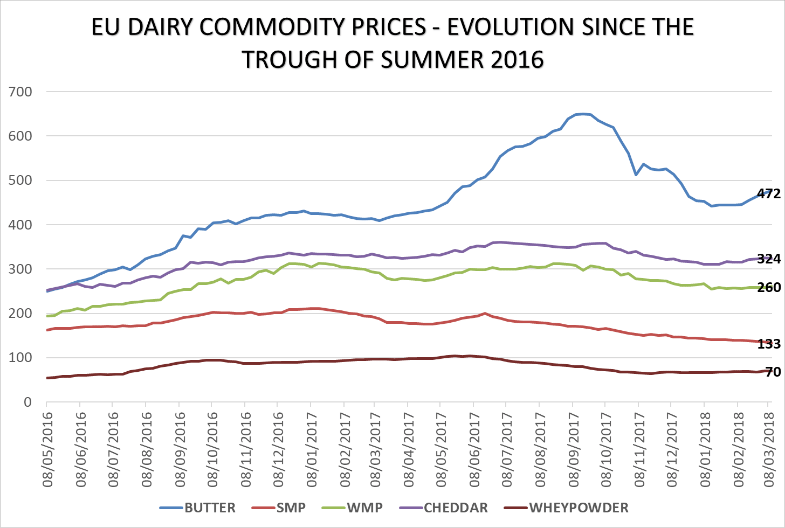

EU dairy commodity prices as reported by the EU MMO have continued to firm. Butter prices have gone up by over €1000/t since January, while SMP has lifted €120/t in the last month (see graph based on EU MMO reports below).

SMP stocks moving at last

SMP prices seem set to recover – though slowly – as intervention stocks are starting to move in earnest at long last.

In the most recent tender, which closed 15th May and was adjudicated yesterday, the EU Commission received bids for 124,360t, with prices offered ranging from €500/t to €1277/t. The minimum price selected by the EU Commission for adjudication was €1155 – €100 above the April tender – which resulted in 41,598t of SMP being sold between the €1155 and the top price bid. In fact, the bids exceeded the amount of product available by around 5,000t (there was insufficient stock of the right age in certain countries relative to the bids within the eligible price range).

This means that, since December 2016, over 76,000t of SMP has been sold out of intervention – of which around 65,000t in the last 2 tenders alone.

The EU Commission is expected to increase the quantities available for the June 19th tender to around 149,000t. It will do so by bringing forward the eligibility date for the stock from product purchased before 1st May 2016 to before 1st June 2016.

Buyers are clearly engaging more with the scheme, and willing to pay more as the fresh market picks up. This is very positive and holds the prospect that a substantial volume of SMP in intervention could be disposed of before year end.

In recent weeks, traders had been pointing out that the EU intervention stock had become largely irrelevant to the fresh market – and this was showing as SMP prices started firming slowly.

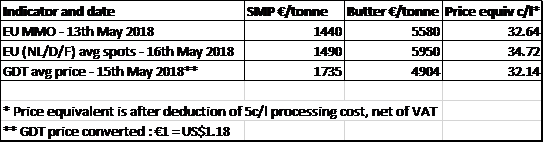

There’s a long way to go, though. With EU average prices (13th May) averaging at €1440 and latest spot quotes (16th May) at €1490, only this week’s GDT price at US$ 2047 (€1734) exceeds the intervention reference price.[/vc_column_text][vc_column_text]Returns inching up

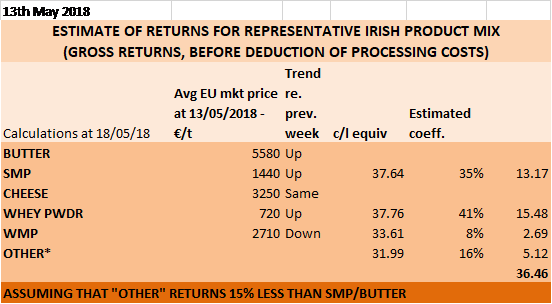

The returns for the Irish product mix, based on EU MMO reported average EU prices, have lifted half a cent per litre in the last week alone. This is largely driven by increases in butter, SMP and whey powder prices.

Based on EU MMO Data

An analysis of the most recent EU average returns, EU average spots from Germany, the Netherlands and France and the latest GDT auction earlier this week, show that these commodity prices would justify stronger milk prices than what is currently being paid by most co-ops (even allowing for the much-appreciated support top ups paid by most).

]The April Ornua PPI, unchanged from March at 100.4 points (equivalent to 29.6c/l incl VAT), shows that returns available to Irish co-ops have at least bottomed out. Many contracts will have been signed forward some weeks/months ago at prices lower than the current spots or market averages.

We would reasonably expect to see some PPI improvements in the months ahead, reflecting fresh contracts being signed at higher prices.

The PPI provided its hedging effect last autumn/winter, when it returned more than average EU prices, and this lag effect is operating the other way – at least for the moment.

![]()

Source: Ornua