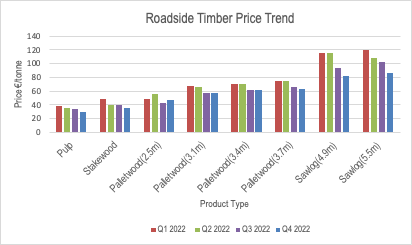

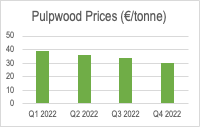

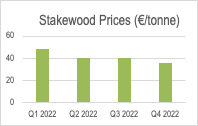

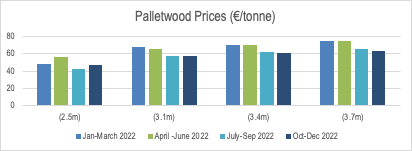

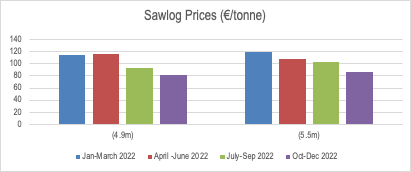

The increase in timber prices in the first half of 2022 experienced a sharp decline from July onwards with the downward trend continuing from October to December last year.

The decrease was a result of lowered demand, partly due to the rising cost of living and reduced construction activity. Timber prices are expected to see some improve in 2023 with reports of increased prices received in January 2023.

The prices quoted in the IFA Farm Forestry Timber Market report were sourced from forest owners, forestry companies and sawmills.

All prices quoted are for Sitka spruce (ex VAT).

Roadside Prices

| Product Type | Length (m) | Diameter (cm) | Price € /tonne (Roadside)* |

| Pulp | 3 m | < 7cm | 25-34 |

| Stakewood | 1.6 m | > 8cm < 15 cm | 35-42 |

| Palletwood | 2.5 m | > 14 cm | 40-54 |

| 3.1 m | > 14 cm | 56-60 | |

| 3.4 m | > 14 cm | 58-63 | |

| 3.7 m | > 14 cm | 60-66 | |

| Sawlog | 4.9m | > 20cm | 80-85 |

| 5.5 m | > 20cm | 82-90 |

Standing Prices

| Standing Prices | Price €/tonne |

| 1st Thinning | 16-20 |

| 2nd Thinning | 18-25 |

| 3rd Thinning | 22-30 |

| Clearfell | 30-65 |

Timber Price Trends (Jan 2022 to Dec 2022)